One of the most common personal finance questions people ask is:

“How much money should I have saved by my age?”

Financial goals can feel confusing because everyone’s situation is different. Income levels, living costs, and personal goals all affect how much someone can save. However, financial experts often provide general benchmarks that can help individuals understand whether they are on track.

These benchmarks are not strict rules. Instead, they serve as guidelines to help people build financial stability and plan for long-term goals such as retirement, investments, and financial independence.

Saving money consistently over time is one of the most important habits for building wealth. Even small amounts saved regularly can grow significantly through the power of compound interest and disciplined investing.

In this guide, we will explore how much money you should aim to save in your 20s, 30s, 40s, and 50s, along with practical strategies to help you stay on track financially.

Why Saving Early Matters

Starting to save early is one of the most powerful advantages in personal finance.

When money is saved and invested early in life, it has more time to grow. This growth happens because of compound interest, which allows investment returns to generate additional returns over time.

For example, someone who begins investing in their early 20s may accumulate significantly more wealth than someone who starts investing in their late 30s, even if the later investor contributes larger amounts.

Early saving provides several benefits:

- more time for compound growth

- reduced financial stress later in life

- greater flexibility in career choices

- stronger retirement security

This is why financial planners often encourage people to start saving as soon as possible.

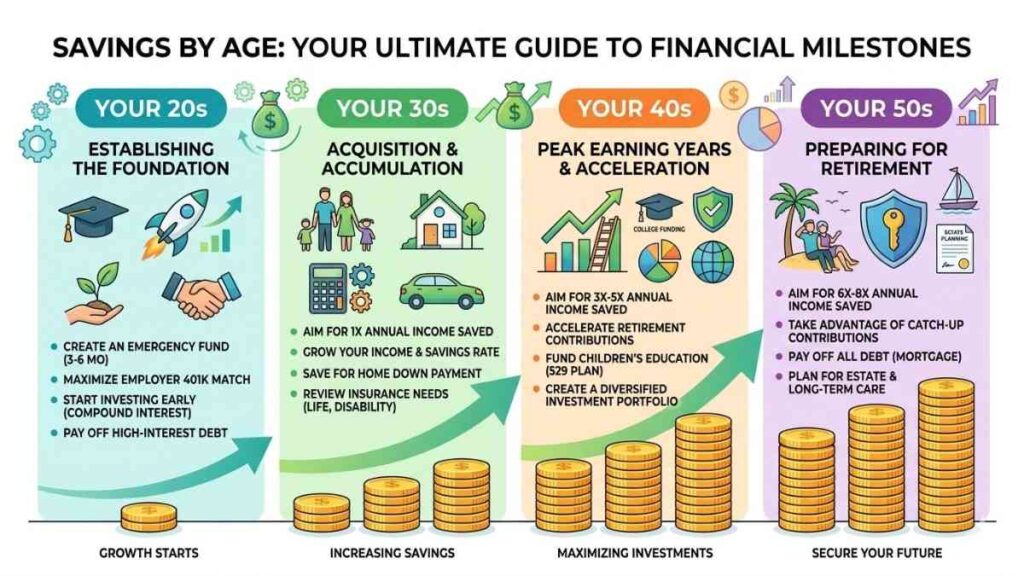

How Much Money Should You Save in Your 20s

Your 20s are usually the beginning of your financial journey. Many people are starting their first full-time job and learning how to manage money independently.

During this decade, the primary focus should be on building good financial habits rather than accumulating large amounts of wealth immediately.

Savings Goal for Your 20s

A commonly recommended benchmark is:

Save at least one year of your annual salary by age 30.

For example:

If you earn $40,000 per year, aim to have approximately $40,000 saved by the time you reach 30.

Financial Priorities in Your 20s

During this stage, focus on:

- building an emergency fund

- avoiding high-interest debt

- learning about investing

- starting retirement savings early

Even small investments made in your 20s can grow dramatically over time.

How Much Money Should You Save in Your 30s

Your 30s are often a time when income increases and financial responsibilities expand. Many people during this stage are managing housing costs, raising families, or advancing their careers.

Because income typically grows during this decade, it becomes easier to increase savings and investment contributions.

Savings Goal for Your 30s

Financial experts often suggest the following target:

Save two to three times your annual salary by age 40.

For example:

If your annual income is $60,000, you may aim to have between $120,000 and $180,000 saved by the end of your 30s.

Financial Priorities in Your 30s

Focus on:

- increasing investment contributions

- building diversified investment portfolios

- managing housing costs carefully

- avoiding lifestyle inflation

This decade can be one of the most important periods for accelerating wealth growth.

Check Your Savings Progress With This Free Calculator

Savings by Age Calculator

Check whether you are on track with your savings based on your age and income.

This calculator gives you a simple estimate based on common savings benchmarks by age. Your actual target may vary depending on your lifestyle, retirement plans, debt, and investment strategy.

How Much Money Should You Save in Your 40s

By the time people reach their 40s, retirement planning becomes more important. This is often the stage when individuals begin evaluating whether their financial progress aligns with long-term goals.

If someone has been saving consistently, their investments may already be growing significantly through compound interest.

Savings Goal for Your 40s

A common benchmark is:

Save four to six times your annual salary by age 50.

For example:

If you earn $70,000 per year, your savings target may fall between $280,000 and $420,000.

Financial Priorities in Your 40s

Important priorities include:

- maximizing retirement contributions

- reducing high-interest debt

- diversifying investment portfolios

- protecting assets through insurance and financial planning

At this stage, many individuals begin focusing on long-term financial security.

How Much Money Should You Save in Your 50s

Your 50s are often considered the final major stage of wealth building before retirement.

During this decade, many people aim to strengthen their financial position to ensure a comfortable retirement lifestyle.

Savings Goal for Your 50s

A widely recommended guideline is:

Save six to eight times your annual salary by age 60.

For example:

If your salary is $80,000, you may aim to have between $480,000 and $640,000 saved.

Financial Priorities in Your 50s

Key financial priorities include:

- maximizing retirement savings

- eliminating remaining debt

- planning retirement income strategies

- protecting investments from unnecessary risk

Proper financial planning during this stage can significantly influence retirement comfort.

Simple Saving Strategy for Every Age

Regardless of age, a simple and consistent saving strategy can help individuals achieve financial stability.

1. Save a Percentage of Income

Many financial advisors recommend saving 15–20% of income.

This includes retirement contributions and investment accounts.

2. Automate Savings

Automatic transfers can move money from income accounts directly into savings or investments.

Automation helps maintain consistency.

3. Invest Regularly

Investing regularly helps build wealth through compound growth.

Diversified investments such as index funds or ETFs are often recommended for long-term investing.

4. Avoid Lifestyle Inflation

Increasing spending every time income rises can slow wealth growth.

Instead, consider investing a portion of every salary increase.

What If You Are Behind on Savings?

Many people worry that they started saving too late.

The good news is that financial progress can improve significantly with disciplined strategies.

If you feel behind, consider:

- increasing your savings rate

- reducing unnecessary expenses

- investing more aggressively (within reasonable risk limits)

- building additional income streams

Even small improvements can create meaningful progress over time.

The Power of Consistent Saving

One of the most powerful financial principles is consistency.

For example:

Saving $500 per month with average investment returns of 8% could grow to more than $700,000 in 30 years.

Increasing monthly contributions can accelerate this process dramatically.

The key lesson is that consistent saving matters more than perfect timing.

FAQ Section

How much money should I have saved by 30?

Many financial planners recommend saving approximately one year of your annual salary by age 30.

How much savings should I have by 40?

A common benchmark is two to three times your annual salary by age 40.

Is it too late to start saving in your 40s?

No. While starting earlier is ideal, consistent saving and investing can still build meaningful wealth.

How much should I save for retirement?

Many experts suggest saving at least 15–20% of income throughout your career.

What is the best way to increase savings quickly?

Increasing income, reducing unnecessary spending, and investing regularly can help accelerate savings.

Final Thoughts

Saving money at every stage of life helps create financial security and peace of mind.

While the exact amount saved by each age may vary depending on personal circumstances, the most important habit is maintaining a consistent saving and investing strategy.

Starting early, investing regularly, and avoiding unnecessary debt can gradually build significant wealth over time.

Financial success does not happen overnight, but with discipline and patience, anyone can improve their financial future.

How to Become a Millionaire from Scratch: A Realistic Wealth-Building Plan for 2026

How Smart Lifestyle Choices Can Save You $10,000 a Year Without Feeling Poor

Read: 7 Smart Investment Options in the U.S. for 2026 (From Safe to High-Growth)

Monthly Budgeting Tips That Actually Work in Real Life

Best Health Insurance in UAE 2026: A Friendly Guide for Expats and Families

Leave a Reply